Las cláusulas ocultas en el seguro comercial que podrían hundirte

Anuncios

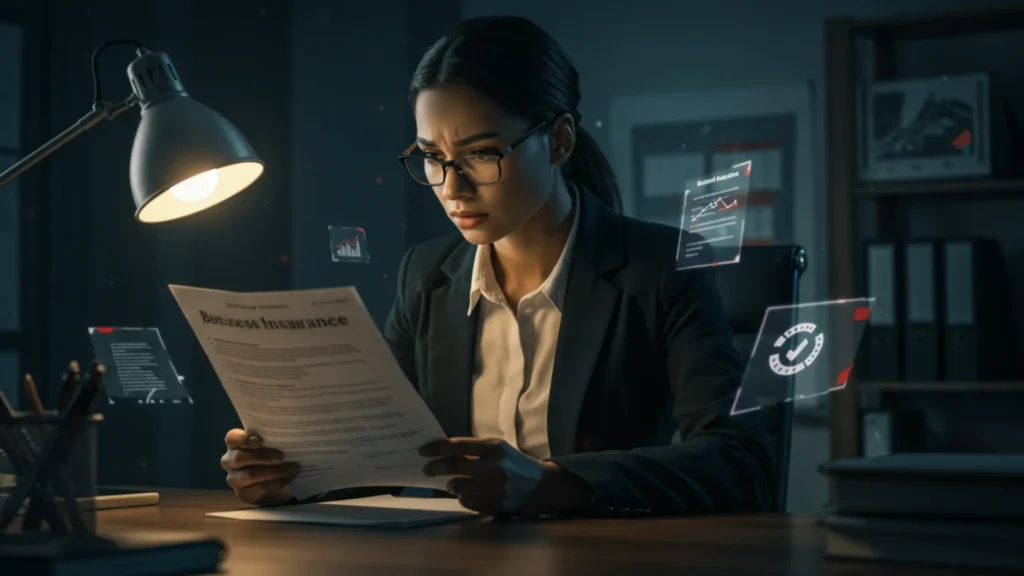

Cláusulas ocultas en el seguro comercial que podrían hundirte El seguro comercial a menudo se considera un escudo necesario, aunque tedioso, contra las catástrofes.

Las empresas invierten miles de dólares, creyendo que sus pólizas ofrecen protección integral contra la ruina. Sin embargo, muchos empresarios aprenden a las malas que el verdadero peligro no reside en lo que cubre la póliza, sino en lo que se asegura meticulosamente. excluye.

La realidad sutil, pero letal, es que la Cláusulas ocultas en el seguro comercial que podrían hundirte Son casi imposibles de detectar sin la ayuda de un experto. Estas exclusiones no son texto de relleno; son trampas impuestas por los suscriptores, que a menudo hacen que una póliza costosa sea prácticamente inútil cuando más se necesita.

Este análisis profundo va más allá de las coberturas básicas. Analizamos las exclusiones más comunes, devastadoras y con una redacción ingeniosa que pueden llevar a una empresa solvente a la quiebra tras la denegación de una reclamación.

Le ofreceremos el conocimiento crítico necesario para auditar su póliza de manera efectiva en 2025. No permita que su red de seguridad se convierta en su máxima vulnerabilidad financiera.

Anuncios

La trampa de la redacción de la póliza: deducibles y depreciación

El impacto inicial de la denegación de una reclamación suele deberse a dos términos financieros aparentemente benignos: el deducible y el plan de depreciación. Estos elementos están meticulosamente diseñados para limitar drásticamente el pago de la aseguradora.

El deducible agregado agravante

La mayoría de los seguros comerciales, en particular los de propiedad y responsabilidad civil general, incluyen una deducible por ocurrencia. Sin embargo, el término más complicado es el deducible agregadoEsta cláusula, a menudo pasada por alto, establece un gasto máximo anual de bolsillo.

Para una pequeña empresa, un deducible de 1TP a 5000 por incidente podría ser manejable. Sin embargo, algunas pólizas imponen un adicional. deducible agregado de $50.000.

Después de diez reclamos menores, es posible que aún esté pagando de su bolsillo, creyendo que su póliza ya entró en vigencia, solo para darse cuenta de que... Cláusulas ocultas en el seguro comercial que podrían hundirte Decidir lo contrario. Verifique siempre si los deducibles se acumulan o se reinician, y comprenda el límite financiero de la póliza para su responsabilidad.

++ ¿Qué tipo de seguro necesitas para una tienda online?

Valor real en efectivo vs. costo de reemplazo

Esta es posiblemente la cláusula oculta más común y financieramente devastadora en el seguro de propiedad comercial. La mayoría de las empresas asumen que su póliza cubre... Costo de reemplazo (CR) el costo real de comprar equipo nuevo o reconstruir una estructura.

Por el contrario, muchas aseguradoras optan por: Valor real en efectivo (ACV)El VCA resta la depreciación del costo de reposición. Si su maquinaria de $100,000 tiene ocho años, su VCA podría ser de solo $30,000, lo que deja un margen de $70,000 que debe cubrir.

Pagas primas durante años, pero la póliza solo cubre el valor residual de tus activos. La diferencia entre el RC y el ACV puede ser el factor decisivo entre la supervivencia y la quiebra para muchas pymes.

Tecnicismos y mantenimiento: la exigencia de diligencia

Las aseguradoras exigen que la empresa cumpla con ciertos estándares operativos para mantener la validez de la cobertura. Las fallas en este aspecto a menudo se aprovechan para denegar reclamaciones por falta de... debida diligencia o mantenimiento adecuado.

H2: La exclusión por “desgaste”

Esta exclusión parece razonable, pero es muy subjetiva. Las pólizas de daños excluyen universalmente los daños resultantes del «deterioro gradual» o el «desgaste normal». Sin embargo, la interpretación de esta cláusula suele ser agresiva.

Por ejemplo, un derrumbe repentino del techo durante una tormenta suele estar cubierto. Si el ajustador de la aseguradora puede argumentar que el derrumbe fue causado principalmente por... fracaso gradual de sellos o signos preexistentes de daños menores por agua o “desgaste”, rechazarán el reclamo por completo.

Esto obliga a la empresa a demostrar que la pérdida fue repentino y accidental, un alto nivel de exigencia probatoria. La interpretación de esta disposición es una de las más significativas. Cláusulas ocultas en el seguro comercial que podrían hundirte.

Lea también: Cómo presentar una reclamación de seguro comercial sin estrés

La cláusula de mantenimiento obligatorio (CMR)

Muchas pólizas comerciales incluyen un RMC que exige programas de mantenimiento específicos y documentados para equipos esenciales como sistemas de climatización (HVAC), generadores y sistemas de extinción de incendios. El incumplimiento estricto de este programa, incluso para una reclamación no relacionada, puede invalidar la cobertura.

Supongamos que una inundación daña su inventario. Si la aseguradora descubre que no se realizó la inspección anual obligatoria de su sistema de climatización (HVAC), podría argumentar que la falta de mantenimiento demuestra negligencia general, lo que complica o incluso deniega la... no relacionado Reclamación por inundación. Esta cláusula convierte en un arma los pequeños descuidos administrativos en perjuicio del asegurado.

Exclusiones operativas: limitaciones al alcance del negocio

Alguno Cláusulas ocultas en el seguro comercial que podrían hundirte limitar directamente cómo Una empresa opera, a menudo sin que el propietario se dé cuenta de que está violando los términos de sus propias políticas simplemente al expandir sus operaciones.

Las limitaciones geográficas y territoriales

Las pólizas de responsabilidad civil general y responsabilidad profesional a menudo especifican lo siguiente: territorio Donde se cubren las actividades comerciales. Para un negocio de comercio electrónico, esto es crucial.

Si su póliza sólo cubre operaciones dentro de los Estados Unidos y usted inadvertidamente vende un producto que causa lesiones en Canadá, el reclamo que surge del incidente canadiense podría ser denegado.

Esto es especialmente cierto para las empresas que emplean contratistas remotos o internacionales. Asegúrese de que la política cubra explícitamente a los empleados y las operaciones realizadas. afuera La dirección comercial principal y el territorio designado. Esta falta de previsión geográfica es una trampa cada vez más común en nuestra economía global.

Leer más: Cómo leer una póliza de seguros como un director financiero

La cláusula mínima de seguridad de datos (seguro cibernético)

El equivalente moderno del RMC es el Cláusula de mínimos de seguridad de datos Se encuentra en casi todas las pólizas de ciberseguro modernas. Las aseguradoras ahora exigen a las empresas que mantengan estándares de seguridad específicos, como el uso obligatorio de la autenticación multifactor (MFA), copias de seguridad periódicas de los datos y capacitación en seguridad para empleados.

Si su empresa sufre un ataque de ransomware y la aseguradora descubre que un empleado clave no tenía MFA habilitada en su cuenta, la aseguradora puede argumentar que la empresa no cumplió con los mínimos de seguridad requeridos.

Esta falla constituye un incumplimiento directo de las condiciones de la póliza, lo que proporciona una sólida base para la denegación de una reclamación, incluso después de años de pagar primas cibernéticas. Esta letra pequeña crítica demuestra cómo Cláusulas ocultas en el seguro comercial que podrían hundirte convirtiendo una capa protectora en una prueba de procedimiento.

Ejemplo: A una empresa de desarrollo de software en Texas se le denegó la cobertura por una filtración de datos de $500,000 porque su póliza exigía parches de seguridad quincenales en todos los servidores. La empresa había aplicado parches cada tres semanas durante tres meses, una pequeña desviación que la aseguradora utilizó para alegar incumplimiento.

El rol del corredor y la agenda del suscriptor

Comprender estas exclusiones requiere reconocer el conflicto de intereses inherente. La función del suscriptor es minimizar el riesgo y el pago, mientras que la función principal del corredor es vender una póliza que parezca integral.

La cláusula de garantía y representación

En la aplicación de la póliza, una empresa realiza representaciones sobre sus operaciones, ingresos y protocolos de seguridad.

La aseguradora incluye una cláusula que establece que estas declaraciones son garantías Verdades absolutas. Si la aseguradora descubre posteriormente que una declaración fue sustancialmente falsa (aunque no intencional), puede anular la póliza. retroactivamente desde sus inicios.

Esto significa que si exageró el tamaño de sus instalaciones o subestimó el uso de materiales peligrosos en la solicitud, un reclamo posterior no relacionado podría ser rechazado por completo.

Esta cláusula de garantía es un acuerdo de alto riesgo, que a menudo resulta ser uno de los más importantes. Cláusulas ocultas en el seguro comercial que podrían hundirte financialmente.

La restricción temporal del “aviso de pérdida”

Toda póliza incluye una cláusula que exige que la empresa notifique a la aseguradora sobre un posible siniestro dentro de un plazo específico (por ejemplo, «lo antes posible» o «en un plazo de 30 días»). Una táctica común de denegación se basa en la interpretación de «lo antes posible».

Si una empresa intenta inicialmente resolver internamente un incidente menor y semanas después se da cuenta de que el daño es grave, la aseguradora podría rechazar la reclamación, argumentando que la empresa no notificó a tiempo. Esto impone al asegurado la responsabilidad de reconocer de inmediato la gravedad del evento, una tarea prácticamente imposible en una situación caótica.

Analogía: Confiar en un seguro comercial estándar sin examinar a fondo las exclusiones es como comprar un paracaídas que luce genial, pero que tiene letra pequeña que indica que no se abrirá si saltas a más de 3000 metros o si la velocidad del viento supera los 48 km/h. Compraste la protección, pero las condiciones la hacen inútil para el mismo escenario para el que la compraste.

Estrategia práctica: Cómo auditar su política ahora

La solución es una revisión proactiva y detallada de las pólizas. Los empresarios deben tratar sus documentos de seguro como un acuerdo financiero crucial, no solo como una carpeta de papeles.

Estadística: Una encuesta realizada en 2024 a pequeñas y medianas empresas (PYME) por una firma de abogados comerciales especializada en litigios de seguros encontró que 45% de denegaciones de reclamaciones Las consecuencias de las pólizas de responsabilidad civil general y de propiedad se atribuyeron a exclusiones específicas pasadas por alto (ACV vs. RC, fallas de mantenimiento o violaciones de garantía) en lugar de a una falta de un tipo de cobertura básica.

La estrategia inteligente es invertir el guion. En lugar de preguntar qué cubre la póliza, exigir saber con precisión qué cubre. excluye.

| Categoría de exclusión | Paso de auditoría de políticas procesables | Por qué esto importa |

| Valoración de activos | Demanda Costo de reemplazo (CR) cobertura por escrito; rechazar el Valor Real en Efectivo (ACV). | El ACV lo deja a usted responsable de años de depreciación, lo que paraliza los esfuerzos de recuperación. |

| Alcance operativo | Verificar Límites geográficos cubrir todo el trabajo remoto, territorios de ventas y ubicaciones de la cadena de suministro. | Una reclamación fuera del territorio definido es una negación automática. |

| Diligencia/Mantenimiento | Obtenga una lista clara de todos Cláusulas de mantenimiento obligatorio (CMR) y documentar rigurosamente el cumplimiento. | Una falta de mantenimiento, incluso si no está relacionada, es una excusa poderosa para la negación. |

| Activador de reclamación | Aclarar en la norma “Notificación de pérdida” qué constituye “tan pronto como sea posible” en días definidos. | El aviso tardío es la táctica de negación más simple y letal utilizada por las aseguradoras. |

Conclusión: Convertir el escudo en una verdadera defensa

La lección más importante para todo propietario de un negocio es esta: debe reconocer que la amenaza más importante para su recuperación financiera no es el desastre en sí, sino la posibilidad de que Cláusulas ocultas en el seguro comercial que podrían hundirte Serán utilizados como armas contra usted.

La verdadera seguridad proviene de comprender meticulosamente las exclusiones y negociarlas. antes Ocurre un evento. Esto requiere una revisión detallada y contradictoria de la póliza con un asesor de seguros o un asesor legal independiente, no solo con su agente de ventas.

Preste atención a la valoración de los activos, los límites geográficos y las responsabilidades operativas. No espere a que se produzca una crisis para descubrir las fallas fatales de su póliza.

Comparta su experiencia o haga sus preguntas más difíciles sobre seguros en los comentarios a continuación. Desmantelemos juntos estos obstáculos en las políticas.

Preguntas frecuentes (FAQ)

P: ¿Puede mi aseguradora rechazar un reclamo si realizo cambios menores en mis operaciones comerciales?

A: Sí, potencialmente. Si modifica su perfil de riesgo empresarial (por ejemplo, al añadir un proceso de fabricación, iniciar ventas internacionales o almacenar nuevos materiales peligrosos) sin notificar ni obtener la aprobación de su aseguradora, esta puede alegar que incumplió gravemente el contrato de la póliza. Esto se incluye en la Cláusula de garantía y representación, lo que hace que la divulgación completa sea de suma importancia.

P: ¿Cuál es la mejor manera de evitar la trampa ACV vs. RC?

A: Solicite siempre que su póliza incluya explícitamente la Costo de reemplazo (CR) aval tanto para edificios como para contenidos (equipos, inventario).

Si la aseguradora se niega debido a la antigüedad de los bienes, sabe que el seguro no cubrirá el costo total de su reemplazo. Nunca dé por sentado que el RC está incluido; confírmelo en la página de declaraciones.

P: ¿Las pólizas cibernéticas cubren las pérdidas por “error humano”?

A: Depende en gran medida de la póliza. Muchas pólizas estándar de ciberseguridad excluyen la cobertura si la pérdida se debió a acciones intencionales o negligentes de un empleado que incumplen un requisito de seguridad obligatorio (como eludir la autenticación multifactor obligatoria).

Aquí es donde el Cláusula de mínimos de seguridad de datos Es crucial. Si el error ocurrió a pesar de los protocolos obligatorios, es más probable que se otorgue cobertura. Si el error se debió a la falta de implementación del protocolo requerido, se espera una denegación.