Financial Deficit: The Cost of Living on Autopilot

Anuncios

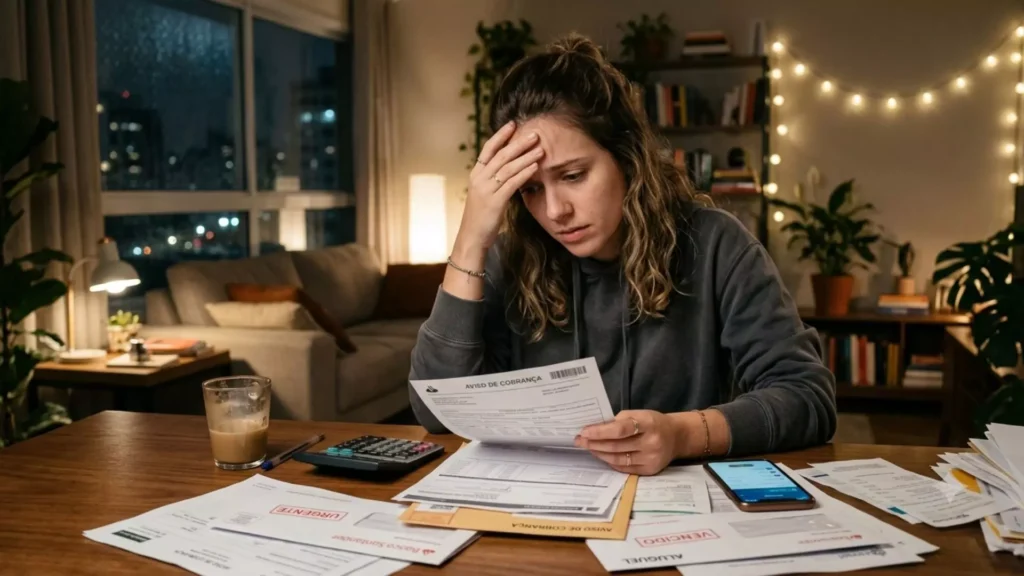

Cost of Living on Autopilot serves as the primary catalyst behind the quiet erosion of modern household stability across major global economies today.

When individuals delegate their financial choices to recurring subscription models and unmonitored digital banking transactions, systematic spending leaks quickly become completely unmanageable.

As economic pressures intensify through 2026, relying on convenience-based financial habits pushes millions of middle-class families directly into severe structural debt.

True financial recovery requires a comprehensive, deep structural understanding of how passive behavioral traits interact negatively with persistent macroeconomic inflationary forces.

Core Insight Overview

- The Silent Leak: Automatic subscription renewals and unmonitored digital payments mask true monthly expenditure totals.

- Inflationary Friction: Macroeconomic price increases cause fixed subscription values to quietly consume personal disposable income.

- Actionable Recovery: Transitioning from passive financial drift to manual budget track controls prevents systemic wealth degradation.

What Causes the Accumulation of a Personal Financial Deficit?

How Do Automatic Payments Distort Real Consumption Awareness?

Relying heavily on digital transaction tools creates a dangerous cognitive disconnect between swiping your device and losing real purchasing power.

Anuncios

When your banking application quietly processes twenty distinct recurring software renewals every month, your brain fails to register the cumulative financial impact.

This psychological detachment turns your wallet into a leaking ship where money slips out before you can even track it.

Consider how easy it is to ignore small, recurring ten-dollar smartphone applications or cloud storage upgrades on your banking statement.

Over a typical fiscal year, these microscopic expenses consolidate into thousands of dollars of undocumented, passive wealth destruction.

This unmonitored drain quickly eats away at your primary savings safety net without your conscious awareness or explicit day-to-day approval.

Why Does High Macroeconomic Inflation Compound Passive Choices?

The structural danger of maintaining a rigid Cost of Living on Autopilot multiplies drastically when global market prices spike unexpectedly.

When utility corporations, insurance firms, and streaming platforms quietly bump their monthly service rates by fifteen percent, passive consumers remain completely oblivious.

Your baseline structural expenses grow larger while your fixed corporate paycheck stays completely stagnant over the exact same period.

A recent Bank of America household spending study revealed that 34% of adult consumers consistently spend more than they earn each month.

This alarming data point underlines how dangerous passive reliance becomes when macroeconomic forces actively adjust the underlying cost of basic goods.

Ignoring small structural price changes over twelve months guarantees a substantial personal budget deficit that eventually requires high-interest credit intervention.

How Does Passive Spending Threaten Long-Term Wealth Preservation?

What Is the Lifestyle Creep Trap for Modern Earners?

When professionals receive a corporate promotion or a salary bump, they typically increase their daily consumption habits automatically.

They upgrade to premium gourmet meal deliveries or shift to luxury gym memberships without establishing clear, long-term wealth boundaries.

This unconscious adjustment ensures that higher income simply fuels higher baseline waste rather than expanding investment portfolios or liquid assets.

Why do we work exhausting hours just to let automatic payment systems empty our accounts before we can save?

This lifestyle creep creates a fragile economic reality where a single unexpected corporate layoff or medical emergency sparks immediate insolvency.

Your fixed overhead remains incredibly high while your primary source of revenue completely vanishes, leaving you stranded with massive liabilities.

++ Errores de fijación de precios que conducen directamente a un déficit

How Does Compound Interest Turn Small Deficits into Financial Disasters?

When your recurring monthly expenses consistently exceed your actual net take-home pay, credit card debt inevitably steps in to bridge the gap.

Carrying a balance of just three thousand dollars at a typical twenty-four percent interest rate triggers a catastrophic wealth-destroying cycle.

The compounding interest charges quickly grow larger than the initial principal debt, trapping your household budget in a permanent financial deficit.

Think of this compounding cycle like a heavy snowball rolling down an icy hill, gathering destructive mass with every rotation.

What began as a few harmless, forgotten media subscriptions evolves into a crushing wall of high-interest consumer debt over time.

Breaking free from this specific trap requires absolute manual control over every single penny entering or exiting your household.

Leer más: Cómo el gasto en productos de conveniencia alimenta el déficit financiero

Why Is Mindful Budgeting the Ultimate Solution for Recovery?

How Does Tracking Your Cash Flow Restore True Economic Agency?

Reclaiming control over your financial destiny demands that you immediately terminate every single automated payment mechanism tied to your accounts.

Forcing yourself to manually review, authorize, and physically execute every transaction reintroduces necessary psychological friction into your daily spending habits.

This conscious step forces you to confront the reality of your consumption choices, instantly eliminating impulsive, low-value retail expenditures.

For example, when you manually write out a bank transfer for a premium gym facility you never visit, you cancel it.

This simple act of active operational review saves hundreds of dollars annually that would otherwise vanish into corporate profit margins.

Active tracking transforms you from a passive passenger into an empowered navigator who explicitly directs where your wealth goes.

Lea también: ¿Por qué las renovaciones automáticas aumentan rápidamente el déficit financiero?

What Structural Budget Frameworks Best Eradicate Unconscious Waste?

Implementing a strict zero-based budgeting framework requires you to allocate every single dollar of monthly income to a specific category.

Under this rigorous system, your total revenue minus your targeted expenses, investments, and savings goals must always equal zero.

This method prevents unallocated cash from drifting into thoughtless retail purchases or forgotten entertainment subscriptions at the end of the month.

By actively assigning a clear purpose to your money, you eliminate the gray areas where lifestyle creep typically thrives.

You begin prioritizing long-term financial freedom over the short-term dopamine hits associated with frictionless, automatic one-click digital purchases.

This disciplined approach serves as an unyielding firewall, protecting your hard-earned wealth from the constant temptations of modern consumerism.

Domestic Budget Architecture Comparison

The data matrix below contrasts the long-term structural impacts of passive financial habits versus active cash flow management.

| Financial Management Variable | Cost of Living on Autopilot | Active Zero-Based Budgeting |

| Transaction Visibility | Low (Hidden behind automatic bills) | High (Every transaction manually logged) |

| Susceptibility to Price Hikes | High (Rate increases go completely unnoticed) | Low (Price adjustments trigger review) |

| Average Monthly Waste Ratio | 12% to 18% of Net Income | Less than 2% of Total Revenue |

| Emergency Savings Stability | Vulnerable (Consistently depleted by leaks) | Robust (Systematically funded every month) |

| Principal impulsor de la deuda | Unconscious subscription and lifestyle creep | None (Spending limited to cash reserves) |

| Long-Term Wealth Growth | Stagnant (Wealth consumed by passive choices) | Exponential (Maximized investment capital) |

Reclaiming Sovereignty Over Your Wealth

Dismantling your Cost of Living on Autopilot is a necessary act of financial self-defense in our fast-paced modern economy.

Leaving your financial choices on cruise control ensures that corporate automated billing systems will steadily drain away your personal wealth.

Transitioning to an active, manual relationship with your cash flow instantly closes structural spending leaks and fortifies your long-term savings.

Ultimately, true economic peace of mind does not stem from how much you earn, but from how intentionally you allocate your capital.

By stepping up to manage your budget consciously, you replace stressful financial deficits with predictable, compounding prosperity.

Take your finances off autopilot today, take the steering wheel back into your hands, and secure the bright future you deserve.

Are you ready to audit your bank statements and eliminate hidden subscription traps this weekend? Share your personal budgeting breakthroughs and experiences in the comments section below!

Preguntas frecuentes

What is the fastest way to identify hidden recurring subscription drains?

Download your last three months of banking statements, highlight every automated charge, and immediately cancel services you have not utilized.

How often should I manually update my household budget tracking sheet?

Dedicate fifteen minutes every single weekend to log your expenses, ensuring your spending patterns align with your monthly goals.

Can automatic bill payments ever be useful for disciplined savers?

Automating your savings transfers and investments is highly beneficial, but automated utility bills still require close, regular manual verification.

Will canceling unused streaming accounts significantly impact my financial deficit?

While a single subscription seems trivial, canceling multiple hidden services saves thousands over time, helping reverse a structural budget deficit.